" height="271.9999926478547px" id="EEb7rlRyU" width="823.9999863254119px"/><path d="M 41.234 82.42 C 64.009 82.42 82.469 63.97 82.469 41.21 C 82.469 18.451 64.009 0 41.234 0 C 18.461 0 0 18.451 0 41.21 C 0 63.97 18.461 82.42 41.234 82.42 Z" fill="rgb(20, 232, 155)" height="82.4204655951471px" id="oKwt2AI3_" transform="translate(545.508 14.698)" width="82.46885142513122px"/></g></svg>)

A critical assessment of the nuclear renaissance – do we need technology breakthroughs?

Nuclear power (from fission) is an established, zero-carbon electricity source and currently supplies approximately 9% of global electricity. As a firm, resilient, (somewhat) dispatchable and extremely safe energy source, it offers continuous generation, effectively complementing intermittent renewables like wind and solar to meet grid demand. Following a surge in construction in Europe and North America during the 1960s and 1970s, new nuclear plant development has largely stagnated worldwide, with notable exceptions in China, Russia, and South Korea. In the West, this slow down can be attributed to minimal or negative demand growth for electricity, as well as construction challenges, differing political and social perceptions of nuclear power in various regions, and the broader transition toward other clean technologies.

More recently, there has been much talk of a so-called nuclear renaissance. Following years of electricity demand plateauing or decreasing in Western economies, demand is beginning to increase due to electrification (EVs, heat-pumps), cooling, and data centre buildout. This clear surge in demand requires a growing supply of clean, firm power. Technologically, nuclear fission is perfect to meet this challenge.

And politicians, policymakers, investors and big tech seem to agree.

US President Donald Trump signed four executive orders in May of 2025 to expedite deployment of next-gen nuclear technologies. His predecessor Joe Biden signed the ADVANCE Act with the aim of inducing the Nuclear Regulatory Commission to lower the barriers for new nuclear projects.

In the UK, in June, the government announced £14.2 billion to the planned Sizewell C power station and £2.5 billion to a new Small Modular Reactor (SMR) programme with Rolls-Royce as the preferred partner.

Big Tech companies have all signed deals with nuclear reactor companies to power their data centres: Microsoft, Amazon and Google have all signed either power purchase agreements or made direct investments. Microsoft has signed a $3b deal with Constellation Energy to reopen the shuttered Three-Mile Island plant. Amazon has signed a long-term PPA with Talen Energy to provide power for it’s data centres from an existing nuclear plant, with a view to building more SMRs in the future, as well as making a direct investment of $500m into X-Energy’s Series C round to fund the development of it’s High-Temperature Gas SMR, the Xe-100. Google has signed an agreement with Kairos Power to purchase power from its SMRs: these are based on advanced molten salt technology that is yet to obtain commercial regulatory approval; construction of a demonstration reactor began in 2024.

VC investment is booming. According to Sightline Climate, $2.3b has gone into the sector in the first half of 2025, nearly matching the total for 2024 ($2.4b), mostly into startups developing micro or small modular reactors. Notable deals include Radiant Nuclear’s $165m Series C in May 2025 (micro reactor for off-grid applications), Natura Resources $20m Series A (molten salt advanced reactor) and Terrestrial Energy (also molten salt) going public via a SPAC.

And the public markets are buoyant too: the share prices of the nuclear fuel and reactor companies Cameco, Oklo, NuScale, Constellation Energy and BWX Technologies are all trading at record highs (as of June 2025).

At Zero Carbon, we are constantly evaluating sectors that require decarbonisation: what are the challenges, where are the solutions and are there any opportunities for technology innovation to have an impact, and for us to generate returns. It is with this lens that we wanted to explore the burgeoning nuclear renaissance, what is the status of nuclear power today, and what do we expect it’s role to be in the future.

A bit of background

The origins of nuclear power lies in early 20th-century scientific breakthroughs, including the discovery of nuclear fission in 1938. This foundational work quickly transitioned from military application, notably the Manhattan Project, to energy generation. The world's first self-sustaining nuclear chain reaction was achieved in 1942 by Enrico Fermi's team, paving the way for the first grid-connected nuclear power plants in the mid-1950s, such as the USSR's Obninsk and the UK's Calder Hall.

The 1960s and 1970s saw a rapid global expansion, particularly in Europe and North America, driven by the promise of affordable and secure electricity. However, this growth significantly decelerated from the late 1970s largely as a result of major accidents like Three Mile Island (1979) and Chernobyl (1986), which profoundly impacted public perception and heightened safety regulations.

Nuclear reactors fall into four main categories. The vast majority of the global fleet today uses Light Water Reactors (LWRs) – or more specifically Pressurised Water Reactors (PWRs) and Boiling Water Reactors (BWRs). They are the most mature and widely deployed, with proven operational history and established regulatory pathways. Due to economies of scale, LWRs have been getting bigger, with an average power output of between 1000 and 1600 MW.

High-Temperature Gas Reactors (HTGRs) use inert gases like helium as the coolant, enabling higher operating temperatures for increased thermal efficiency, passive safety features, and the potential to provide high-grade industrial heat. Their commercial deployment remains limited (there are two 100 MW systems operating in China, and a test reactor in Japan), but the potential for industrial heat makes them attractive.

Liquid Metal Cooled Reactors (LMRs), using sodium or lead as the coolant, are championed for their compact designs, high power density, and efficient operation. They also have the ability to exploit a fast neutron spectrum for fuel breeding or more effective waste transmutation; the challenge lies in managing the chemical reactivity of the sodium metal coolants. There are two operational reactors in Russia, and one test reactor each in India and China.

Lastly, Molten Salt Reactors (MSRs) employ liquid salt as both fuel and coolant, with inherent safety advantages, high thermal efficiency, and the potential for greater fuel flexibility, including the ability to consume existing nuclear waste. They are the least mature technologically and face complex material corrosion challenges.

There are currently no commercially-available advanced (non-LWR) reactor types in the US or Europe.

The argument for advanced nuclear

The argument for nuclear power, especially in the context of increasing electricity demand, is compelling. It is a clean, firm power source that does not rely on weather conditions. Its high capacity factor means it generates power almost continuously, and its minimal land footprint is an increasingly attractive feature in land-constrained regions. The electricity is generated via turbines, which means that nuclear power plants offer grid inertia, a crucial stability service. Once built, the operating costs for nuclear power tend to be low and driven by personnel: nuclear power plants provide highly skilled, high-paying jobs. While the

Levelised Cost of Energy (LCOE) for traditional nuclear is often higher than renewables—Lazard’s latest LCOE for US nuclear is $141-$228/MWh vs. $50-131/MWh for utility-scale solar + storage or $44-123/MWh for wind+storage—these unique grid benefits could, in principle, justify a premium.

It’s also one of the safest forms of electricity: specifically it is 800 times safer than coal in terms of the number of deaths per unit of energy produced (that’s including the deaths at Chernobyl and Fukushima).

A key part of the "renaissance" narrative centres on advanced nuclear technologies, particularly Small Modular Reactors (SMRs). These promise to address many of the historical barriers. Their modularity allows for factory fabrication and assembly, potentially reducing overall project costs, making financing easier, and speeding up construction. This modularity also opens doors for new business models and applications, such as providing industrial heat for heavy industries, where decarbonisation is particularly challenging.

Proponents suggest SMRs could also expedite regulation. Their standardised, smaller designs, coupled with enhanced passive safety features that rely on natural forces rather than active systems, could theoretically simplify the licensing process. Other benefits include a reduction in waste volume and increased fuel efficiency, which, in principle, would further reduce costs across the lifecycle.

The argument against nuclear

To be clear, in making an argument against nuclear fission technologies, I am not claiming that to deploy nuclear technology would not be impactful. Indeed, the world’s climate would be in better health had more countries followed France’s strategy of the 1970s to get over 60% of it’s electricity from nuclear power, following the oil shock of 1974; nuclear power has an emissions intensity of just 6 gCO₂e/kWh, compared to the global average of 445 gCO₂e/kWh today.

The traditional misgivings about nuclear: namely safety and nuclear waste management are becoming less of a concern globally. Germany began a phase out of it’s nuclear power after the Fukushima disaster—although the policy had been established some time before—citing safety concerns as the driving force. And in reality, although radioactive and with long half-lives, the volume of nuclear waste produced is vanishingly small compared to fossil equivalents. For more information on nuclear waste disposal and common misconceptions – see this explainer from the World Nuclear Association.

It’s just that it’s not clear that nuclear fission is the best choice to provide clean, firm, safe power affordably. Indeed all recent efforts in Western economies provide evidence to the contrary. Projects are overbudget, overtime (=overbudget) and take ages to deploy. Why not just build alternative sources of clean firm power—renewables + storage, geothermal, tidal power—instead? Let’s take a look.

Almost all nuclear projects run over budget. According to analysis by Professor Bent Flyvbjerg—expert in megaprojects and author of How Big Things Get Done—97% of nuclear power projects are over budget, over half of those are over budget by more than 150% – with the average cost overrun for these being 300%. Compare this to solar projects where 39% are overbudget, but only 2.44% have a cost overrun greater than 150%.

A big driver of being over budget is being behind schedule. The large budgets for nuclear power plants require debt financing, and as timelines start to slip, the cost of financing (particularly in a high interest rate environment) can escalate dramatically. For example, the Vogtle Units 3 & 4 in Georgia in the US were originally projected at $14 billion for a 2016-2017 completion. The cost surged to over $30 billion, entering service in July 2023 and April 2024. In the UK, the Hinkley Point C project's estimated costs have already ballooned from an initial £18 billion to up to £43 billion. Commercial operation was initially targeted for 2025 and is now projected for 2029-2031. And at Flamanville 3 in France which began in 2007 with an estimated €3.3 billion and a 2012 completion, the project saw its cost climb to €13.2 billion, with some estimates reaching €22.6 billion including financing. It finally connected to the grid in December 2024, approximately 12 years behind schedule. Lazard’s data shows that nuclear power costs are the most sensitive to interest rates.

Why does this happen?

Nuclear safety is paramount, leading to incredibly stringent and often evolving regulatory frameworks. New regulations or interpretations can emerge during the long construction phase, leading to costly design modifications, additional safety features, and re-licensing efforts, sometimes termed the ‘regulatory ratchet’

We don’t have the skilled workforce required. This means that each new project often functions as a ‘first-of-a-kind’ (FOAK) or a highly customised build, even if based on an existing design. This prevents the benefits of standardisation, mass production, and ‘learning-by-doing’ that typically drive down costs in other industries. Instead, many Western countries have experienced a negative learning curve, where expertise is lost between projects, leading to lower productivity and increased costs.

The long hiatus in new builds in many Western countries has led to the atrophy of specialised nuclear supply chains

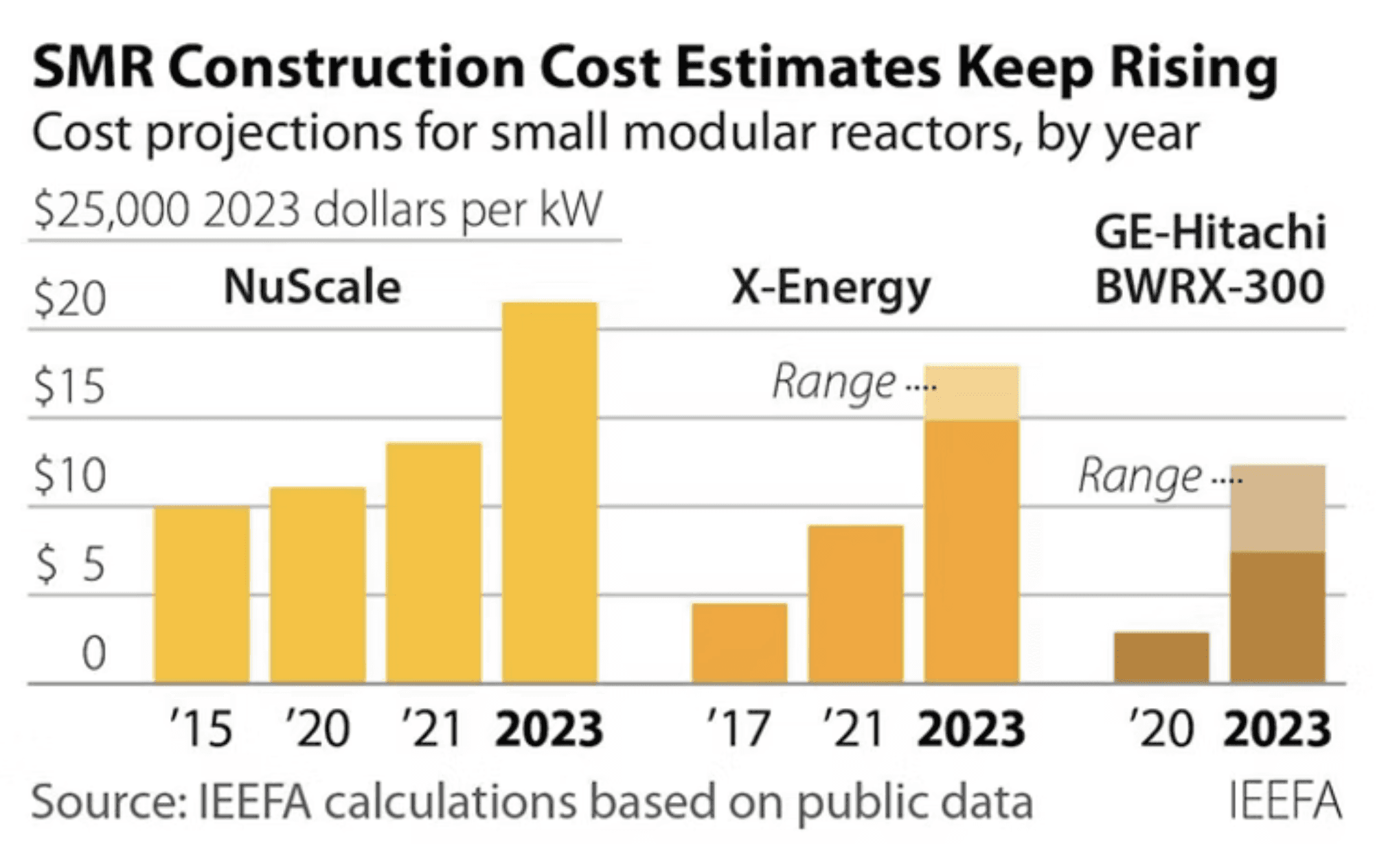

Despite the promise of SMRs in enabling Nth of a kind nuclear facilities to bring down the cost. They also face the challenges of diseconomies of scale: they are most expensive per kW than GW-scale reactors to start with (the US department of Energy Pathways to Commercial Liftoff Report for Advanced Nuclear estimates a median cost of $13k/kW median cost for SMRs vs $8.5k/kW for large reactors). And their estimated costs keep on rising. Unlike state-backed models in China and South Korea where the government often bears significant financial risk, Western projects typically rely on private financing, exposing them to the full brunt of these escalating costs and delays.

SMR construction costs are higher than conventional nuclear per MW, and continue to increase vs. estimated costs. Source: Joe Romm

And ultimately, the higher upfront costs for nuclear result in higher costs for ratepayers, whether paid for directly via the utility (as in the US) on via the wholesale markets because of energy costs. According to the Georgia Public Service Commission: the resulting price of nuclear energy will be five times that of solar plus storage in the region, per MWh.

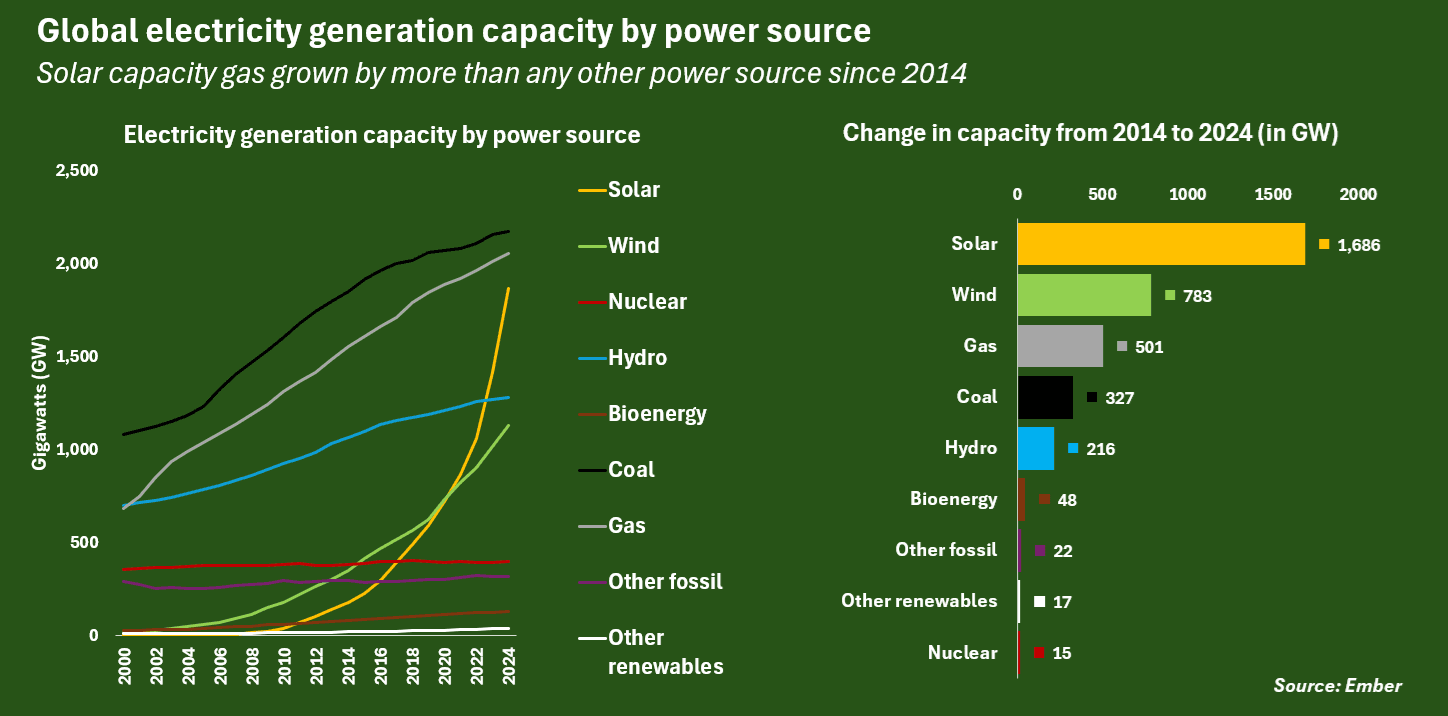

We have better options. The energy generated from solar power is set to overtake the amount from nuclear power for the first time in 2025, whilst the decreasing cost of lithium-ion batteries is enabling firming of renewable resources for less that the cost of nuclear. They are built on schedule, on budget and fast: the estimated lead time for solar and wind projects is 41 months and 50 months, respectively. In the UK since Hinkley Point C (3.62 GW, operational 2030) started construction in 2017, the UK has installed 14 GW of wind capacity and 3.75 GW solar capacity.

Geothermal technology innovations are advancing rapidly, and could offer a lower LCOE option that is faster to deploy (current geothermal installations also have long permitting timelines, but there is scope to reduce timelines as technologies mature).

Solar capacity set to overtake nuclear for the first time in 2025. Source: Data from Ember via Reuters

What is needed to accelerate nuclear deployment? Or bring down the cost?

Accelerating nuclear deployment and significantly reducing its cost hinges on fundamental shifts in licensing reform and a substantial improvement in engineering and project management expertise. The former is primarily a regulatory challenge, while the latter is a direct product of the scale and experience within the sector's workforce. Neither of these critical levers can be addressed solely through venture capital funding, though a broader groundswell of support and available capital can certainly provide momentum.

At Zero Carbon Capital, we’ve come to the conclusion breakthrough technological innovation isn't the primary requirement to accelerate nuclear fission. Existing nuclear technologies are mature, and even advanced designs are likely to proceed via incremental improvements, subject to the slow, meticulous approval processes of (rightly) cautious regulatory bodies. This makes it challenging for us to identify transformative opportunities where our early-stage capital could be truly impactful, and perhaps it is simply too capital intensive for a pre-seed fund like ours.

Crucially, our assessment leads us to conclude that nuclear fission, in its current Western deployment model, isn't a strategic fit for us as a fund. While startups could theoretically tackle areas like permitting, specialised training, or recruitment to enhance efficiency, these aren't the areas where venture capital currently seems to be flowing; instead, most VC investment targets novel reactor technologies, which are unlikely to significantly accelerate near-term deployment or cost reduction. Furthermore, we're not convinced that nuclear, given its historical challenges and current economic profile, represents the optimal solution for clean, firm power when compared to other emerging options. As a result, we believe our focus is best directed towards other areas where technology innovation can more effectively accelerate the decarbonisation of electrical supply, such as tidal power, geothermal, long-duration energy storage (LDES), and grid optimisation. We remain committed to backing startups in these spaces, like our portfolio companies Vema Hydrogen, AED Energy, Ionate and Porpoise Power.

If you would like to continue the conversation, or have a technology solving some of these problems, please get in touch!

Contact: chloe@zerocarbon.capital

References & recommended reading

https://www.energy.gov/lpo/pathways-commercial-liftoff-reports

https://www.samdumitriu.com/p/infrastructure-costs-nuclear-edition

https://rogerpielkejr.substack.com/p/how-much-does-it-cost-to-build-a

https://www.sustainabilitybynumbers.com/p/nuclear-construction-time

https://world-nuclear.org/nuclear-reactor-database/summary

https://www.ctvc.co/europes-nuclear-power-shift-247/

https://www.responsiblealpha.com/post/is-the-nuclear-renaissance-a-myth

Acknowledgements

I am grateful to all the experts and founders who shared their time and insights with me on this topic, any errors in the text are of course, mine. Thank you to Bruno Chesnay (International Atomic Energy Agency), Aaron Chote (Climate Connection), Mai Ly (Regen Ventures), Mike Edmonson (UK National Nuclear Laboratory), Guy Cohen (Sightline Climate), Vera Kunz (Apex Ventures).