" height="271.9999926478547px" id="EEb7rlRyU" width="823.9999863254119px"/><path d="M 41.234 82.42 C 64.009 82.42 82.469 63.97 82.469 41.21 C 82.469 18.451 64.009 0 41.234 0 C 18.461 0 0 18.451 0 41.21 C 0 63.97 18.461 82.42 41.234 82.42 Z" fill="rgb(20, 232, 155)" height="82.4204655951471px" id="oKwt2AI3_" transform="translate(545.508 14.698)" width="82.46885142513122px"/></g></svg>)

Innovations to close the copper supply-demand gap.

12 min read

Copper metal has been critical to humankind’s development since the Bronze Age around 3000 BC. It is the third most widely used metal by mass (after iron and aluminium), and its excellent conductivity makes it a crucial component of electrical wiring, electric devices and other domestic and industrial applications.

It’s no wonder then, that the energy transition to renewables and electrification will require large amounts of additional copper: to build out electricity infrastructure, for electric vehicles—a typical EV requires 83 kg of copper vs 23 kg for an ICE vehicle—as well as wind turbines, solar panels, and so on. General economic development in the global south and AI-driven data centre growth are also expected to increase demand. Projections suggest that demand is set to grow from ~26 million tonnes (Mt) per year in 2024 to around 35 Mt in 2035. The capital requirements for this level of expansion are estimated to be ~$250 billion (compared to the $150 billion invested in the preceding ten years).

The copper market today

Copper is mined in various regions around the world, with Chile, Peru, China, and the Democratic Republic of Congo being the top producers. Chile accounts for ~25% of global copper production, and in return the copper industry accounts for 20% of Chile’s GDP. Major mining companies like BHP, Freeport-McMoRan, Glencore, and Codelco dominate the industry, operating large-scale mines and processing facilities worldwide. The diversification of copper supply means that copper isn’t always considered a critical mineral (BGS, EU, US), and there are, in principle enough reserves of copper globally in order to meet demand.

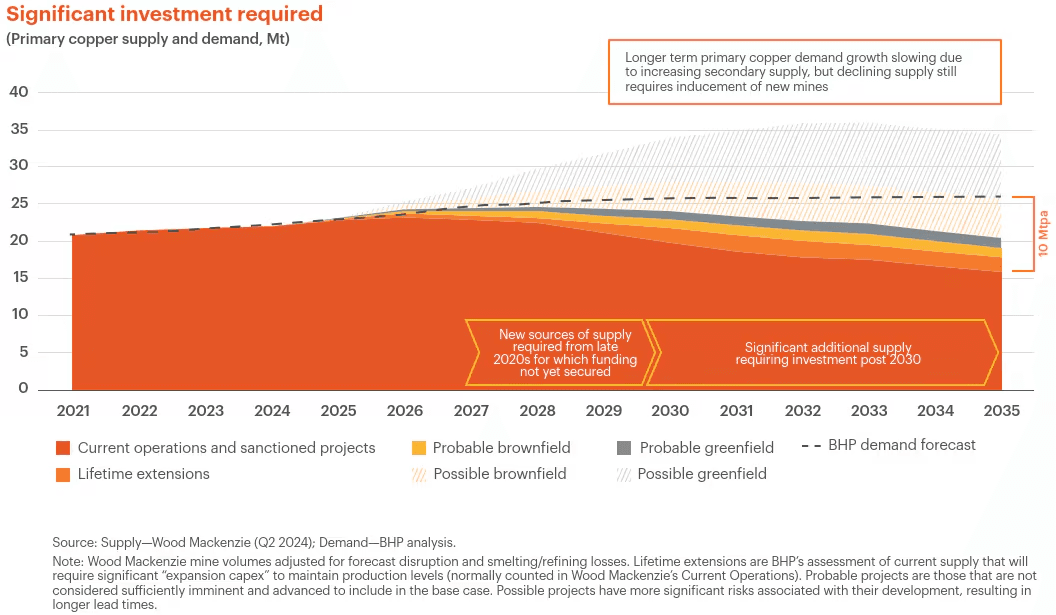

Despite this, the copper market faces significant challenges to meet this demand and a projected 10 Mt shortfall is expected by 2035, which could negatively impact global electrification and emissions reduction targets. Current projections of supply from major copper producers are no higher than today and the average time taken to open a new mine from discovery of a deposit to operation is over 16 years, so the ability to ramp up supply quickly is limited. This could lead to increases in copper prices and copper price volatility.

Projected supply-demand gap for copper based on current operations and probably future assets being developed. There is expected to be a 10 Mtpa shortfall. Source: BHP

Every part of the typical lifecycle of a copper mine is becoming more challenging:

Exploration is inefficient and capital intensive: less than 1% of discoveries result in a mine being built. High grade deposits are harder to find, and exploration budgets are being cut, with miners preferring to further develop existing brownfield sites.

Declining ore grades are making extraction and processing more expensive.

Lengthy permitting processes extending deployment times as environmental considerations are coming to the fore, despite faster build tiems

Copper production today

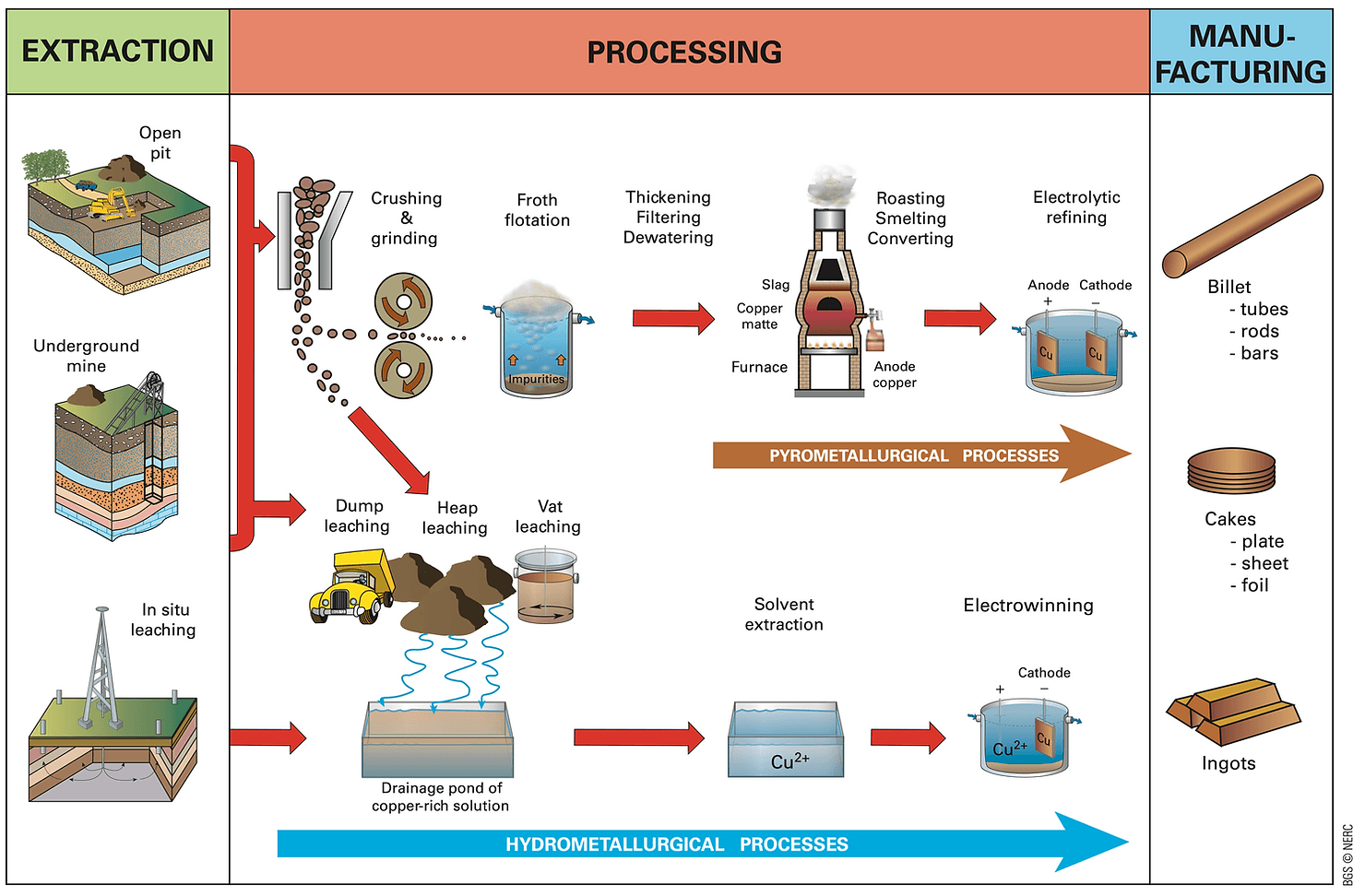

Copper production involves several stages, from mining to processing and refining. The two main methods of copper extraction are pyrometallurgy (around 80% of produced copper today) and hydrometallurgy, each with its own set of processes.

Open-pit mining is the most widely used technique for copper extraction today, accounting for about 90% of copper mines globally. It is used when copper deposits are located near the surface. Underground mining is employed when copper deposits are too deep for open-pit mining and involves creating shafts or adits (horizontal tunnels) to access the ore body and then blasting the ore and transporting it to the surface via shafts or tunnels. After extraction, the ore undergoes comminution: crushing and grinding the ore to reduce the particle size.

Pyrometallurgical extraction of copper from its ore involves burning copper concentrate in a furnace to remove impurities. Copper concentrate is made from copper ore via what is known as froth flotation: a process to progressively increase the copper content from as low as 0.5% in the ore to over 30% in the final concentrate. After smelting, the copper is then further refined to produce copper at 99.99% purity. Although the concentration usually happens at the site of the mine, most smelting facilities are located in China, where there has been significant investment in these high CAPEX sites.

Hydrometallurgy is particularly suitable for oxide ores, and involves leaching (dissolving copper using acidic solutions, often sulfuric acid), followed by solvent extraction and electrowinning (SX-EW). Solvent Extraction (SX) involves separating copper from the leach solution using reagents including organic solvents, and electrowinning is the electroplating of copper from the purified solution onto cathodes. The SX-EW process produces high-purity copper cathodes without the need for smelting or refining. Traditional hydrometallurgical processes account for 20% of copper production, but only copper oxide ores are amenable to sulfuric acid leaching and SX-EW. High grade copper oxide deposits have largely been depleted, with lower grade sulfide ores now prevalent as mines get deeper.

The stages of copper production from extraction to manufacturing. The pyrometallurgical process currently supplies ~80% of copper demand. Even though the hydrometallurgical process is generally less emissions intensive, it is currently most suitable for oxide ores, whereas copper reserves are dominated by sulfide-based ores. Source: BGS NERC

Environmental impact of copper production

Copper production is an energy-intensive process with significant environmental consequences. The average industry emissions stand at 4.1 tonnes of CO₃ per tonne of copper, resulting in overall emissions on the order of ~100 MtCO₂e/year. Energy consumption ranges from 24-37 GJ per tonne of copper cathode, with the mining, grinding, smelting, and electro-winning being the most energy-demanding processes. These high energy requirements translate directly into CO₂ emissions, although many companies are looking to reduce diesel consumption and emissions by electrifying mining vehicles and increasing the use of renewables at their mining sites. Smelting typically produces sulfur dioxide as a by-product which leads to local pollution and acid rain (but is also used to produce the sulfuric acid for leaching the copper oxide ores).

Water resources are also a concern. The industry is water-intensive, with a typical mine consuming up to 170 tonnes of water per tonne of copper produced, with copper in general being more water-intensive than other critical metals. Beyond consumption, water pollution presents severe risks through acid mine drainage and tailings management. Tailings failures lead to groundwater contamination which can affect local ecosystems and communities. Add to this the land and habitat destruction that are inherent to copper extraction, particularly in open-pit mining where a single large mine can span nearly a mile in diameter and several thousand feet deep. Both of these aspects contribute to negative sentiments that can impact whether a company obtains the social license to operate and therefore whether mining permits are approved or not.

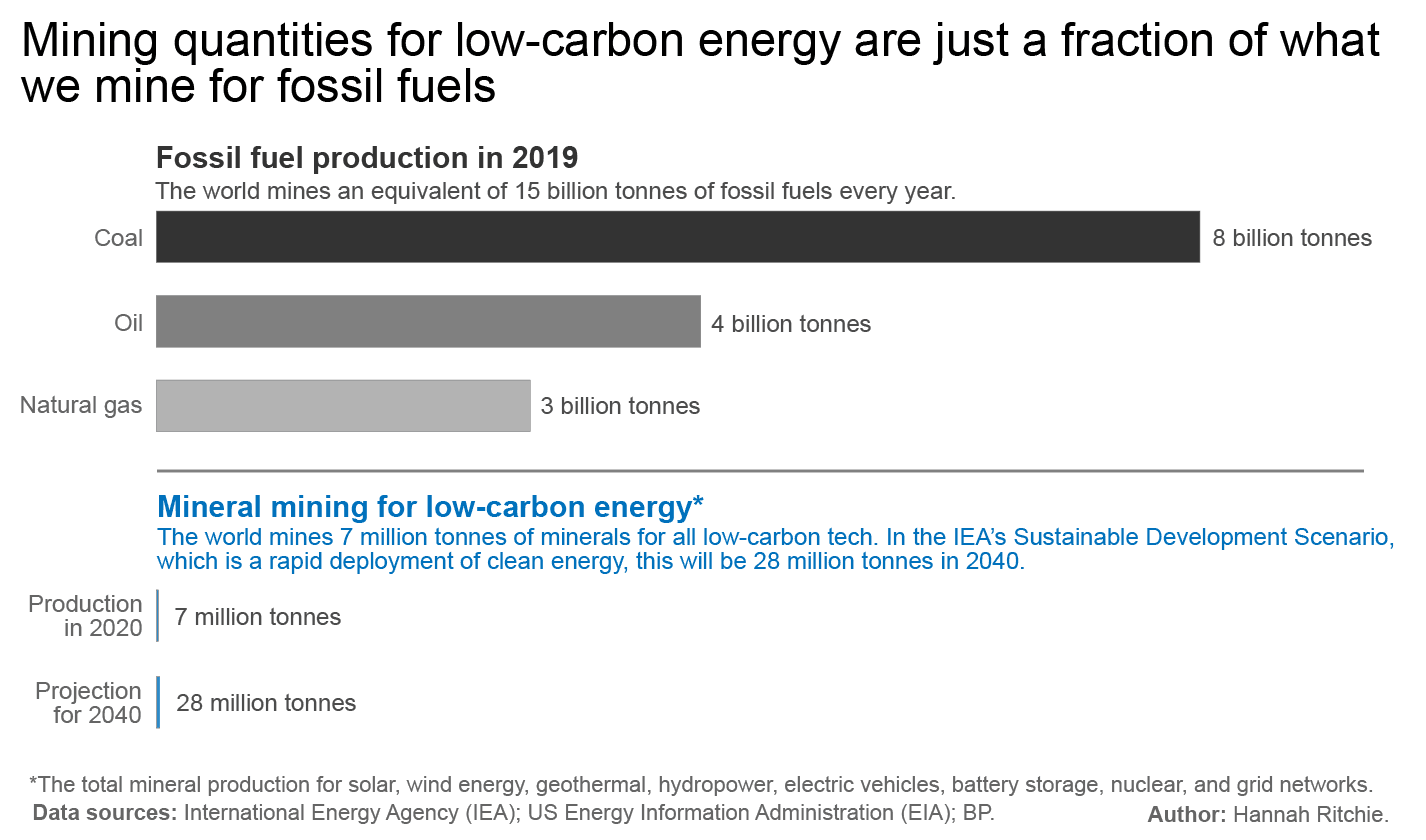

The mining industry—including copper mining—faces the difficult challenge of having to ramp up supply of materials for the energy transition, as well as decarbonising its own operations, and doing so in a way that is least impactful on the environment. And whilst mining has a bad reputation, let us not forget that the mass of minerals we need for the energy transition is but a fraction of the coal we are currently mining.

Mining quantities for mineral mining vs fossil fuel production. Source: Sustainability by Numbers

The hydrometallurgical SX-EW process generally incurs lower costs and environmental impacts, while smelting remains advantageous for processing high-grade sulfide ores and recovering precious metals. The major challenge is that sulfide ores are not amenable to sulfuric acid leaching in the same way as oxides - they form an impenetrable ‘passivation layer’ which prevents leaching.

Meeting the supply–demand gap

Can we increase secondary (recycled) copper supply?

To an extent. Copper recycling is relatively straightforward and recovery and recycling rates could be increased. The main constraint is the lifetime of copper in products—since copper is typically in use for over 20 years, the maximum copper available will be the amount mined 20 years ago, which won’t be enough to meet our growing demand. Even with increases in copper recycling there is predicted to be a 10 Mt deficit in 2035.

Can we reduce demand?

The two main ways of reducing demand are via thrifting (using the least amount of copper to get acceptable performance) and substitution. Since aluminium is cheaper than copper it can be considered as a substitute—but its inferior conducting properties mean that 3x as much aluminium is needed to replace the same amount of copper wiring. Substitution is unlikely to play a big role unless copper more than doubles in price.

Can we speed up permitting?

In an effort to increase supply security in Europe, the EU passed the Critical Raw Materials Act (CRMA) in April 2024. For the 17 strategic metals it stipulates a number of targets including 40% of materials processing to be performed in the EU and 25% from recycling and 10% of extraction derived from the EU. In order to achieve this it is also introducing a streamlined permitting process to expedite approvals and reduce mine development timelines. Improvements to environmental standards and community engagement are also mechanisms by which to obtain the social license to operate that would improve permitting timelines.

Can we de-risk the exploration process?

Exploration—the systematic process of searching for and evaluating mineral deposits for potential economic extraction—involves several stages, from initial reconnaissance to detailed assessment of mineral resources. But exploration success rates are decreasing, despite an increase in exploration budgets. Of the 239 copper deposits discovered between 1990 and 2023, only 4 occurred in the years 2019-2023.

Companies are combining proprietary exploration data with existing geological surveys and machine learning models to improve exploration success rates; Kobold Metals is the most well-known of these. Others include EarthAI, VerAI, MinersAI. BHP also have a dedicated accelerator, BHPXplor, to fund exploration-focused companies: exploring new territories or employing novel technologies.

Can we improve mine productivity?

One way to avoid exploration costs and permitting timelines is to continue mining existing assets. But this comes at a cost. The high grade oxide ores are found at the surface, and ore grades tend to decline and the mine gets deeper, and deposits are dominated by primary sulfide ores like chalcopyrite which are refractory—that is, they become harder to extract using the more environmentally-friendly leach methods. 70% of remaining reserves are made of this chalcopyrite (CuFeS₂) ore. The next section gives an overview of current technology developments and startups innovating to (i) exploit primary sulfide ores, (ii) improve mining efficiency by reducing energy requirements, and (iii) reduce environmental impacts by e.g. reducing water usage or habitat destruction.

Novel grinding technologies

Novel grinding technologies are emerging to address the energy-intensive nature of traditional comminution processes. The grinding of rock to sizes suitable for further processing currently accounts for 30-40% of mining energy use. New innovative approaches aim to reduce energy consumption, increase efficiency, and improve overall productivity in mineral processing. I-ROX are a startup pioneering pulsed power comminution to dramatically reduce the energy required.

Advantages:

Significant reduction in energy consumption

Improved particle size distribution for downstream processes

Potential for dry grinding, reducing water usage

Barriers:

High initial capital investment

Limited large-scale demonstrations

Mine sorting technologies

Mine sorting technologies leverage advanced sensors and data analytics to separate valuable ore from waste rock early in the mining process. These technologies aim to improve resource efficiency and reduce the environmental footprint of mining operations. Startups in this space include NextOre, Comex, and MineSense.

Advantages:

Increased efficiency in ore processing

Reduction in energy and water consumption

Improved head grade to processing plants

Barriers:

High upfront costs for implementation

Complexity in integrating with existing mine operations

Variability in ore characteristics affecting sorting efficiency

Bioleaching

One type of biomining is bioleaching. Microbes can play many different roles in mining with different modes of action and business models, including oxidation, accumulation commonly used for gold mining and remediation, respectively. Bioleaching has been used to extract copper from sulfide ores; extremophile microbes that are found natively in copper deposits can be harnessed to leach the copper ions from the ore whilst withstanding the acidic pH.

These microbes can be cultivated at the mine site in a bioreactor and added to the ore heap to stimulate leaching. Their ability to act at ambient temperatures can save on energy costs (OPEX), but reaction rates are slow and microbial activity can be difficult to control throughout the pile, due to varying composition, temperature, nutrient distribution etc.

First identified in the 1950s, there was a wave of innovation in biomining in the 2000s and 2010s, but the technologies never went mainstream, and investment in smelters dominated (particularly in China, and such that there is now an overcapacity). Despite publishing 80+ patents on biomining, Codelco’s dedicated biomining subsidiary BioSigma was closed down in 2017, following a drop in the copper price from $4.50 in 2011, to ~$2 in 2016 (copper prices are now back above the $4 mark). Now innovation in biomining is on the rise again, with startups exploiting advanced genomic technologies and modelling to optimise the microbial and/or nutrient composition for the given ore at a given site.

Advantages

Lower energy and low OPEX

Environmentally friendly process

Ability to extract metals from low-grade ores

Can be used for remediation

Barriers:

Slow

Unfamiliarity of miners with biotech

Must be tweaked for different ores/sites

Potential groundwater contamination

Advanced chemical leaching

Non-biological sulfide leaching technologies are also being developed, the most promising of which exploit chloride ions via hydrochloric acid as a leaching agent. Chloride ions are unfavourable for microbial populations in the ores, so cannot be used in conjunction with bioleaching. These chemical leaching technologies benefit from not relying on bioreactors, and can use seawater or brackish water, reducing freshwater pressure. (Mines in Chile are increasingly turning to desalinated seawater as their water supply to reduce water resource pressure). Examples of companies exploiting advanced catalytic methods include Antofagasta and their Cuprochlor method, Chile-based Ceibo, and Jetti Resources, who are partnering with mining majors to deploy their technology, including at the Freeport-McMoran-owned El Abra mine in Chile.

Advantages

Faster than bioleaching

High recovery rates

Can use seawater or brackish water, reducing freshwater pressure

Potentially lower capital costs compared to traditional methods

Barriers

Corrosion issues due to chloride ions

Environmental concerns related to chloride use

Risk of groundwater contamination

Solvometallurgy

Solvometallurgical methods are aiming to do away with using water altogether, with the aim of using benign, low-cost organic or ionic solvents with high affinities for copper ions. Although currently at an early stage of development (TRL 5) this approach should simultaneously lower the environmental impact and improve extraction efficiencies. One of the leading companies in this space is pH7 Technologies.

Advantages

Reduced water requirements

Potential for higher selectivity in metal extraction

Lower energy consumption compared to traditional methods

Barriers

Early stage technology

Supply chains for highly specific chemicals less establisheds

Potential environmental impacts of organic solvents

Emerging electrochemical technologies

There are a number of startups employing distinct electrochemical technologies, including, for example, catalytic electrochemical processing of concentrate. Such processing would enable on site processing of concentrate using renewable energy and bypass the SO₂ emissions generated by smelting. Other approaches including electrochemical membrane filtration processes to enable low energy separations of the metal ions of interest.

Advantages

Potential for on-site processing using renewable energy

Reduction in SO₂ emissions compared to smelting

Potential for high selectivity in metal separation

Barriers

New processes in mining flowsheet can be challenging to commercialise with incumbents

High initial capital costs for implementation

Potential energy intensity of the process

Limited large-scale demonstration of the technology

Less invasive mining

Two technologies aim to reduce the land footprint of mining are in-situ mining and surgical mining. In-situ mining (or in-situ recovery, ISR) involves pumping a lixiviant (leaching fluid) under ground and extracting the pregnant leach solution directly, rather than removing the rock before leaching. It is currently widely used in uranium mining. Electrokinetic in-situ recovery combines in-situ mining techniques with the addition of underground electrodes and application of an electric field to leaching via improved ion migration, currently being developed by Ekion Technologies.

Surgical mining targets small deposits of high grade ores, by extracting the target ore more precisely, almost like a giant syringe. Improved sensing and modelling can make surgical mining more economic—this is the approach taken by Novamera, for example. These more targeted approaches can be more environmentally friendly, by reducing habitat destruction and reducing the energy requirements for digging and grinding or traditional mining

Advantages

Can exploit high grade ores that would not be economical for a large scale traditional copper mine

Potentially reduced permitting times

Lower water consumption

Reduced waste rock and tailings production

Barriers

Unlikely to provide enough copper for the transition

Limited applicability to certain geological formations

Potential groundwater contamination risks with ISR

Public perception and regulatory challenges

The innovators

To make an impact in this space, startups will need to partner with mining companies, to access ore samples to prove out their technology and to have pilots up and running as proof of concept. Any new technologies must be compatible with existing flowsheets of mining operations. The large mining corporates can be slow moving and so project development from lab concept to commercialisation can be a long and CAPEX-intensive journey.

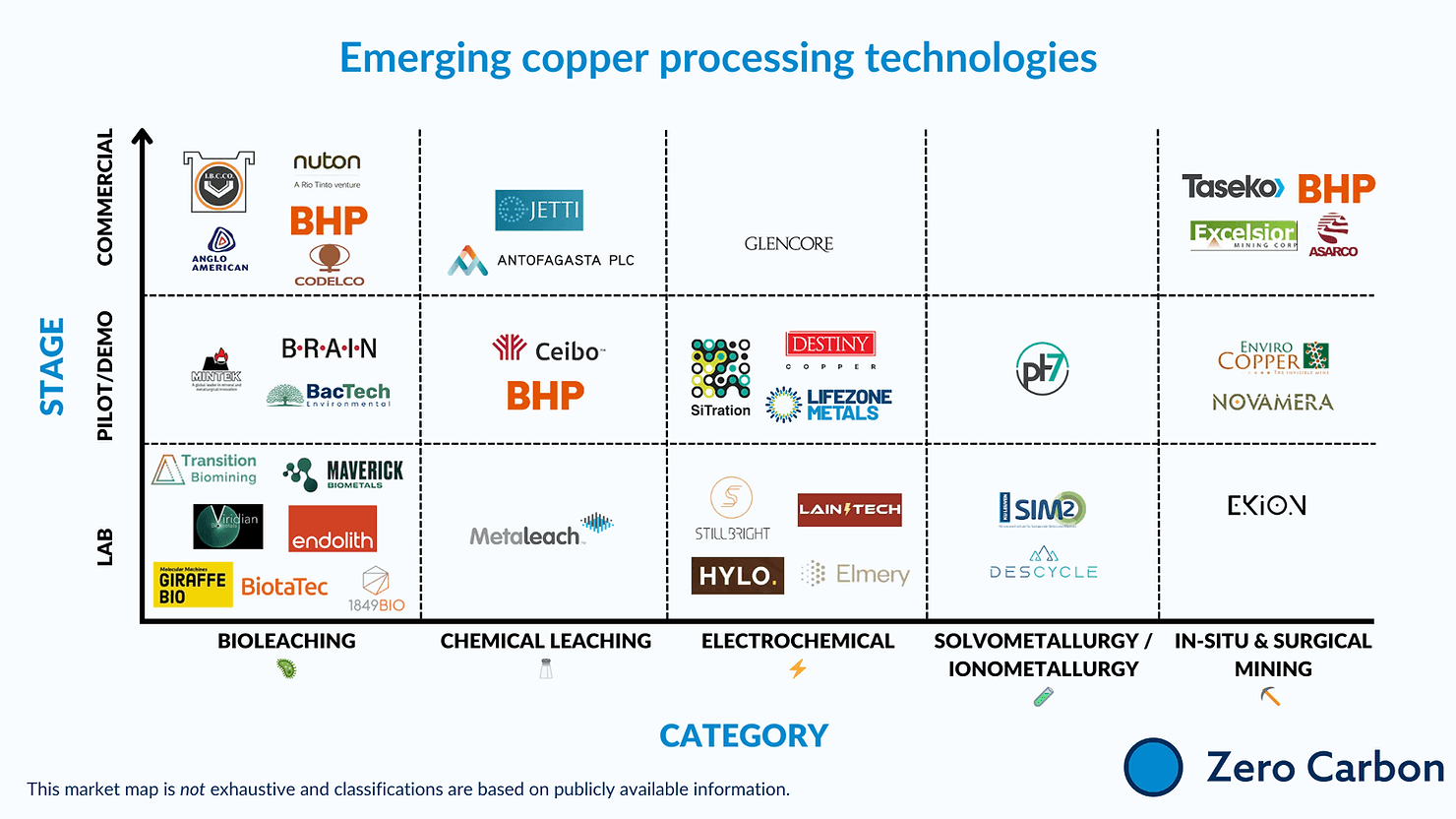

Overview of some emerging technologies for increasing copper mine productivity. This map is not exhaustive. Source: ZCC analysis.

A copper supply-demand gap is looming, and it’s clear that both new technologies and favourable policies will be critical to bridging this gap. Ore grades are decreasing—copper reserves are dominated by low grade and refractory chalcopyrite—and miners are under pressure to reduce the impact of the sector on water stressed regions and ecosystems. Here we’ve given a brief overview of some candidate copper processing technologies to improve the productivity of existing mines. By turning to these technologies with high recovery rates, that are less resource intensive (think water/energy/land), the sector might be able to meet the demand required for the energy transition, and do so in a sustainable way.

If you would like to continue the conversation, or have a technology solving some of these problems, please get in touch!

Contact: chloe@zerocarbon.capital / max@zerocarbon.capital

References & recommended reading

The Electric Vehicle Market and Copper Demand, IDTechEx (2017)

Global Critical Minerals Outlook 2024, International Energy Association (2024)

UK 2024 Criticality Assessment, British Geological Survey (2024)

The Role of Critical Minerals in Clean Energy Transitions, International Energy Association (2021)

New major copper discoveries sparse amid shift away from early-stage exploration, S&P Global (2024)

Commodity Profile: Copper, British Geological Survey NERC (2009)

Understand your copper emissions, Carbon Chain (2023)

A Critical Raw Material Supply-Side Innovation Roadmap for the EU Energy Transition SystemIQ (2024)

BHP Insights: how copper will shape our future, BHP (2024)

Progress in bioleaching: part B, applications of microbial processes by the minerals industries, F. F. Roberts and A. Schippers, Appl Microbiol Biotechnol. 106, 5913–5928 (2022)

The World Copper Factbook, International Copper Study Group (2024)

Acknowledgements

We would like to thank those who took their time to share their insights with us including Madeleine Luck (Quadrature Foundation), Alfred Lam (Chrysalix Venture Capital), Alexandra Iljadica (BHP Ventures), Carmen Falagan (University of Portsmouth), Pilar Parada and Patricio Martinez (Centro de Biotecnología de Sistemas UNAB), Isabella Fandrych (Nucleus Capital), Jack Kennedy (Founders Factory), Tara Ryan (Minviro), Ryan Finlay (Ekometall GmbH).