" height="271.9999926478547px" id="EEb7rlRyU" width="823.9999863254119px"/><path d="M 41.234 82.42 C 64.009 82.42 82.469 63.97 82.469 41.21 C 82.469 18.451 64.009 0 41.234 0 C 18.461 0 0 18.451 0 41.21 C 0 63.97 18.461 82.42 41.234 82.42 Z" fill="rgb(20, 232, 155)" height="82.4204655951471px" id="oKwt2AI3_" transform="translate(545.508 14.698)" width="82.46885142513122px"/></g></svg>)

Spinouts and success, a VC view on spinout equity.

6 min read

The amount of equity a university should take is a controversial issue, and can be challenging to negotiate for founders. The aim of this article is to help prospective scientist founders in universities who are looking to spin out and to help them understand

what investors are looking for

how to set their company up for success

We will use the UK as a starting point for examples, but the general principles are universal. (And we would love to learn more from our European colleagues).

The purpose is not to criticise Universities or their Technology Transfer Offices (TTO), nor to pit investors against TTOs. In fact there has been a lot of dialogue between investors and universities over the past few years, with meaningful collaboration in the form of TenU University Spin-out Investment Terms (USIT) Guide as an important starting point.

That’s not to say that we haven’t seen some horror stories, helped founders negotiate with TTOs, and had to be creative with cap-tables to undo unfavourable equity distribution. But a smoother, low friction process would help TTOs spin out more companies, enable investors to back those companies, and result in more successes.

Investor expectations

Founders, investors, and universities are all (mostly) aligned in wanting to create generation-defining companies that solve big problems. In our case, at Zero Carbon we’re committed to investing in transformative technologies for decarbonisation. The universities’ remit is somewhat broader, with health and life sciences spinouts as a particularly successful output of UK universities.

In a high-growth startup, most of the value of the company is in the future: the success of the company relies on execution and the hard work of the brilliant founders, not simply IP or an excellent academic track record. And in order to be sufficiently incentivised & remain in control, the founders need to have the majority of the equity. Crucially, equity is not a reward for past input. (Alex has written about common cap table mistakes previously here).

Whilst the role of universities in generating IP is undeniably important, it is just one piece of the puzzle. Perhaps universities and TTOs want a ‘good deal’ on their spinouts, in the shape of high pre-investment equity stakes. Universities usually have a policy on equity that is dictated to the TTO who then either negotiate that down with the spinout founders, or stand firm to the policy. But there is a growing understanding that the deal itself is not the end goal, that it represents just the start of the long journey to building a massively successful and impactful company. After all, a 50% stake in a company worth nothing (because it could never get investment) is worth a lot less than 5% in a unicorn worth over a billion pounds!

What do we expect at ZCC?

≤10% equity for the university

The USIT guide recommended 10-25%. We previously voiced our concern that this range is too high.

≤10% equity for academic founders who are staying on as advisors

It is not appropriate to disproportionally reward someone for past work. They may get rewarded already via licence royalties on the patent.

In our experience investing in startups with a range of origin stories, including spinouts from universities, if more than 10% equity goes to non-participating entities it becomes very challenging for that company to raise capital from top tier investors, or in some cases any investors at all. This significantly reduces the chances of success for the company. Investors like to see founders incentivised and also like to be able to buy equity in startups at market comparable valuations. There is little margin for this when more than 10% equity is owned by non-participating founders at incorporation.

It’s important to remember that founders take a huge risk in building a company, usually taking lower salaries for extended periods of time with the risk of not getting a payout if the company fails. Equally, VCs risk investors’ capital to invest in startups. If VCs aren’t able to buy sufficient ownership in companies, they are not able to generate the returns to their investors and their business model fails.

A university’s success, on the other hand, is not solely dependent on the equity stake it takes in spinouts–in fact a university is likely to reap more rewards from the number of spinouts, and ultimately the amount of successfully commercialised IP, than the their spinout equity stake. Universities benefit significantly from the start-up ecosystem that can grow around the university; the startups provide a positive feedback loop with researchers and scientists staying in the area, becoming a hub for sector-specific expertise, graduate employment and so on, think Silicon Valley, or Cambridge Science Park.

In 2021/22, UK universities made £244 million from licensing intellectual property, and only £86 million from sales in shares, which equates to 0.8% of annual research expenditure from sales of shares. The government’s independent review highlights that both sources tend to be driven by a small number of large successes. Streamlining the spinout process should increase the numbers of spinouts and the chances of a large success.

The evidence is there to show that lower equity stakes translate to increased start-up formation, and greater success

And data reveals that spinouts with lower university equity stakes at incorporation are more likely to be successful, according to a study published in 2023 by Beauhurst and the Royal Academy of Engineering, based on UK spinouts between 2011-2023.

Some interesting findings:

In 27.6% of university spinouts, the university takes no equity

In 56% of spinouts the university took a low stake of less than 15%, and 15% took greater than 40% equity stake.

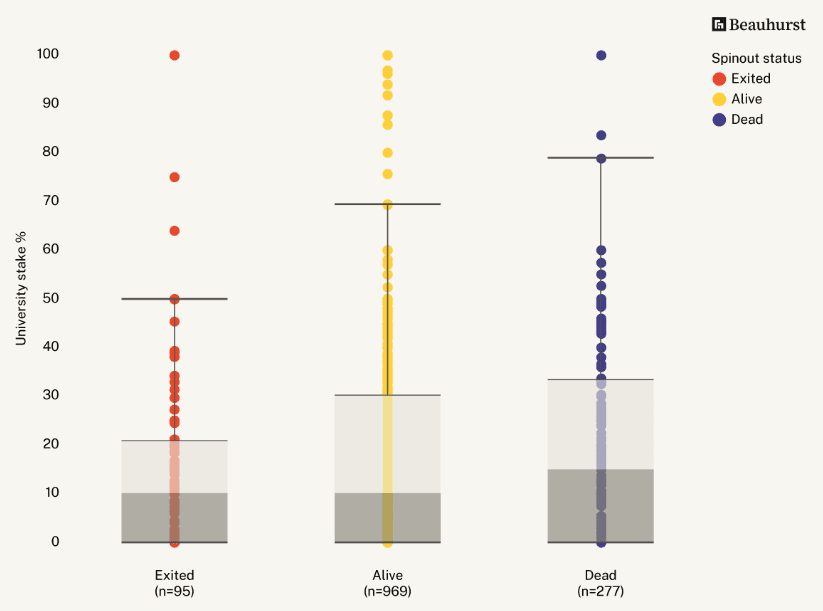

Dead spinouts have higher median university stakes (15%) than exited and active spinouts (10%)

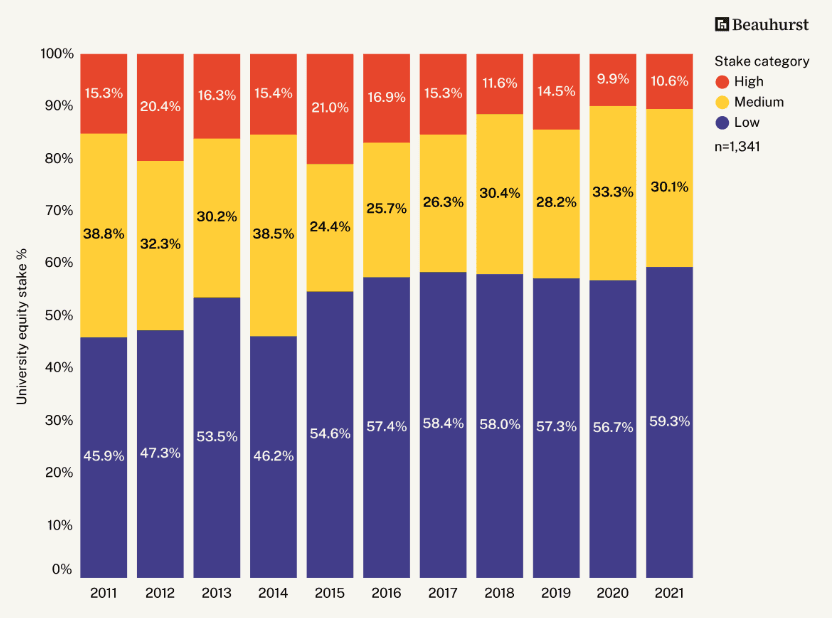

Since 2011, the proportion of universities taking a low stake (<15%) has increased from 46% up to 56%

Typical university equity stakes are coming down: Distribution of university stakes (2011–2021) where a low stake is less than 15%, a medium stake is between 15% and 40%, and a high stake is greater than 40%. Source: RAEng

Spinout outcomes and equity stakes: the data are shown as a box plot which displays a dataset's distribution through five key data points: the minimum, first quartile, median, third quartile, and maximum while highlighting outliers. Dead spinouts have higher median university stakes than exited and active spinouts. Source: RAEng

Whilst there isn’t a direct correlation that says the smaller the stake, the more successful the company will be, but there is a correlation between giving away too much equity at the start and higher failure rates. A smaller stake for the university puts the founders in control.

Change is occurring

Credit where credit is due: many TTOs and universities are adapting and engaging in constructive dialogue with founders and the investor ecosystem, to achieve their aims of spinning out more high-growth companies.

Average equity stakes are coming down: in their latest “Spotlight on Spinouts” report Beauhurst revealed that the average equity stake had decreased to 16.1% in 2024, the lowest in the last decade. There is some way to go, but were going in the right direction.

Tech transfer offices are working together

The SETsquared Impact-IP Deal Readiness Toolkit is an excellent example of University Tech Transfer Offices collaborating to streamline the commercialisation process for all parties.

Groups of TTOs are coalescing around guidance, both in terms of equity terms as well as standardising IP assignment, the USIT guide is an example of this.

The USIT guide recommended 10-25%. We previously voiced our concern that this value is too high. Anecdotally it seems that most university TTOs we have spoken to are proposing the lower end of 10%–this is really good news for the future of UK spinouts.

Cambridge already takes a median equity stake of 8.8%

In conclusion, the data increasingly suggests that universities taking lower equity stakes in spinouts correlate with greater success. While university IP and support is crucial, the future success of a spinout hinges on the founders' execution and hard work. A balanced cap table, where founders retain control and motivation, is vital for incentivising them and attracting further investment. Fortunately, the trend shows that universities and TTOs are adapting, with average equity stakes decreasing and more collaborative efforts emerging. This shift towards lower equity stakes and standardised processes bodes well for the future of university spinouts, paving the way for more impactful, high-growth companies to emerge and tackle the world's pressing challenges.

Of course, the equity agreement is only a part of the negotiation between a spinout and a university; we will be sharing our thoughts on licence agreements and royalties in a future post!

Have you spun out a company from a university? Are you a TTO? Are you in the process of doing this in another European company? Let us know your thoughts!

Further reading:

Mapping equity: a closer look at university stakes in academic spinouts since 2011 Royal Academy of Engineering & Beauhurst (2023)

Spotlight on Spinouts: UK academic spinout trends Royal Academy of Engineering & Beauhurst (2025)

The biggest Cap Table mistakes and ways to avoid or fix them Zero Carbon Capital (2023)

Breaking down the UK negotiation on spinout terms for scientist founders, Wilbe (2023)

Independent review of university spin-out companies Department for Science, Innovation and Technology (2023)