" height="271.9999926478547px" id="EEb7rlRyU" width="823.9999863254119px"/><path d="M 41.234 82.42 C 64.009 82.42 82.469 63.97 82.469 41.21 C 82.469 18.451 64.009 0 41.234 0 C 18.461 0 0 18.451 0 41.21 C 0 63.97 18.461 82.42 41.234 82.42 Z" fill="rgb(20, 232, 155)" height="82.4204655951471px" id="oKwt2AI3_" transform="translate(545.508 14.698)" width="82.46885142513122px"/></g></svg>)

The biggest Cap Table mistakes and ways to avoid or fix them

8 min read

Written in collaboration with Yair Reem from Extantia

In the exciting world of startups, we often get swept up in innovative ideas, growth strategies, and disruptive technologies. However, behind the scenes, there's an unassuming document that quietly plays a crucial role in a startup's journey: the capitalisation table, or "cap table".

This simple spreadsheet, outlining who owns the equity in a startup, can dramatically influence a company's potential for success. It’s not just about numbers; it’s about aligning the company toward growth through motivating executives and enabling high quality decision-making.

It’s easy for decisions made early in the company’s journey to have a significant negative impact on the cap table. In fact, we regularly see companies that have great tech and a great team tackling a big important problem, but where the capital structure is not at all aligned with their future success. Those situations suck for everyone involved. Existing investors are less likely to be left holding onto really valuable stock in the long run; the management team may feel undervalued and experience high-churn; and new investors may be scared off or require onerous terms or recapitalisation to invest. Ultimately, it limits the potential of the company.

Let’s dig into each of these areas, understand why they are important, what “good” looks like, and the mistakes that can cause you headaches in the future.

Motivating the executive team

In a high-growth startup, most of the value of the company is in the future. It needs to be built by the people running the company, and those people need to be able to make the trade-offs, both personal and professional, to make that happen.

Unfortunately, most startups do not generate the sort of revenue that could pay big salaries and bonuses for key executives, so a key aspect of motivation, retention and remuneration is ownership. Of course, your mileage may vary, but most investors look for the executive team to own at least 50% of the equity after the Series A round, to ensure that they maintain significant motivation even after the dilution of later rounds.

Sounds easy right? You own all of the company when you start and you progressively sell bits of it to new shareholders as you grow while ensuring you maintain that magic number at Series A. The trouble arises when you make early deals that leave too much of the company in the hands of passive shareholders. We call this “dead equity”.

There are a few categories of “dead equity” that we regularly see taking up a bunch of the cap table oxygen:

Dormant founders

Many startups have founders on their cap table who were incredibly important to the start of their story but will not be involved heavily in its future. Perhaps they decided to leave, or perhaps they were a co-inventor of some of the underlying tech but decided to stay on in their research position at a university. There are a ton of reasons (good and bad) to be in this position.

Universities

If the startup is spun out of a university, there may be a portion of the equity owned by the university or the university’s investment fund. Without these universities and their research departments, the startup may never have existed, but in most cases their ability to help grow the startup declines with time.

Accelerators / incubators / venture builders

Just like universities, these programs can be critical to the early progress of a startup and to their success in the years immediately after attendance. But over time their impact will reduce and new investors that can provide more going forward support will take their influential role.

Business Angels

Angels are often the first source of cash in a startup providing the initial impetus to get the ball rolling with equipment of employees. But, on the whole, angels will not play a big role in building the future of the company and usually they cannot keep investing (with some obvious exceptions to prove the rule).

It’s conceivable that (and we have seen) these four categories of shareholders own a significant portion of the company before any institutional money is taken on board. While it’s important that their equity adequately rewards them for the role in getting the company where it is now, it’s also really important that the appropriate equity share is given to those that will build the (much larger) future value of the company. Every investor's share of equity should be a balance between how they have contributed up to now and how they will contribute in the future. At odds with human nature, the weight of that split should highly favour the future value.

Here are a few numeric examples and practical advice:

A dormant founder shouldn’t have more than 5%. From the get-go, have a reverse mechanism to assure that someone who is leaving is not holding on to the lion share of her/his shares. Try to buy them out if possible (you can actually defer the cash payment to an exit day).

Universities shouldn’t get more than 10% of equity. If you are also paying royalties then the equity portion should drop below 5% or even to zero. No matter what the equity holding is, it should ALWAYS be subject to normal dilution in future financing rounds. For info on deals people are getting from other universities checkout spinout.xyz.

Accelerators shouldn’t have more than 5% and you should avoid having lots of them on your cap table. The exception to the rule is venture studios that actively take part in the foundation of the company. And even then, they shouldn’t have too much (ideally less than 15%) as at some point the management team is taking over and creating the future value.

Angels - these are coming at pre-seed stage usually. They shouldn’t have more than 15%. Most importantly: never ever give them any actual or de-facto veto rights (more on that in the next item).

Enabling high quality decision making

As with all companies, shareholders in a startup get a say in the way it is run. Every shareholder on the cap table is a potential voice in the decisions that a company makes. It's crucial to ensure that these voices can act together to contribute positively to the company’s future and align around the company’s strategy for creating value.

In a clean cap table, the majority of the equity is owned by the people who are driving the company forward: the executive team and currently active investors. This configuration helps streamline the decision-making process, allowing the company to react quickly and make key strategic decisions fast.

Again, early decisions on equity and voting allocation can make this much more difficult. Some examples we have seen are:

Fragmentation

If a company has taken lots of small checks from angels or small funds and hasn’t really settled on a lead investor with significant share (say 15%) to represent the investor body, then it can be difficult to get the level of consensus needed to pass a resolution. To illustrate, imagine three VCs each owning about 10% of the company, with each one at a different stage in their fund's lifecycle (and fundraising), trying to agree on whether to accept an exit offer or not. You really need to have someone in the lead.

Concentration

The opposite of fragmentation, if a company has sold a significant stake (say 20% or more) to a single investor and that investor is not deeply involved in the future success of the company (including future funding rounds) then new investors may be concerned about whether their voices will be heard over this one loud one. It gets even worse, if you sold over 30% to a seed investor, let alone cases where someone took over 50% of the company.

Super-voters

Even smaller stakes can hold significant power, particularly if those shareholders have been granted special rights, such as veto rights over major decisions. These rights can slow down or obstruct decision-making processes, and they can be a significant deterrent to new investors who don’t want to deal with the hassle of navigating around them.

Time-zones

Founders are often glad to have investors from various corners of the globe. The belief is that this diverse investor base can aid the company in entering new markets and securing additional capital. However, what founders frequently overlook is the impact this "global exposure" will have on their daily lives, not to mention the implications for the company itself. Imagine needing to review a draft contract. By the time your investors on the West Coast wake up and examine the document, those in Japan are already heading to bed. A precious day is lost in the process.

Our overall advice for keeping cap table clean for decision making is:

If you can, pool smaller investors decision-making rights to make for easier voting processes. In cases of conflict of interest, they can still vote seperatly, but you would avoid herding cats.

Avoid getting over concentrated with a single investor too early in your journey, particularly if (like many angels) they can’t dedicate the long-term time or resources to make your company successful.

Don’t grant veto-rights or supernumerary voting powers (unless there is an exceptionally good reason to do so).

Read the fine print, count shares and do the math to calculate which majoriteis are required for which decisions (like raising a new round). Most of time, investors are not asking for veto rights, but are getting a de-facto veto right beacuse someone didn’t do the math. Check, double check, and on the day of signing, check again. One more share can make a difference.

Until you reach Series B, aim to have a maximum of two time zones on your cap table.

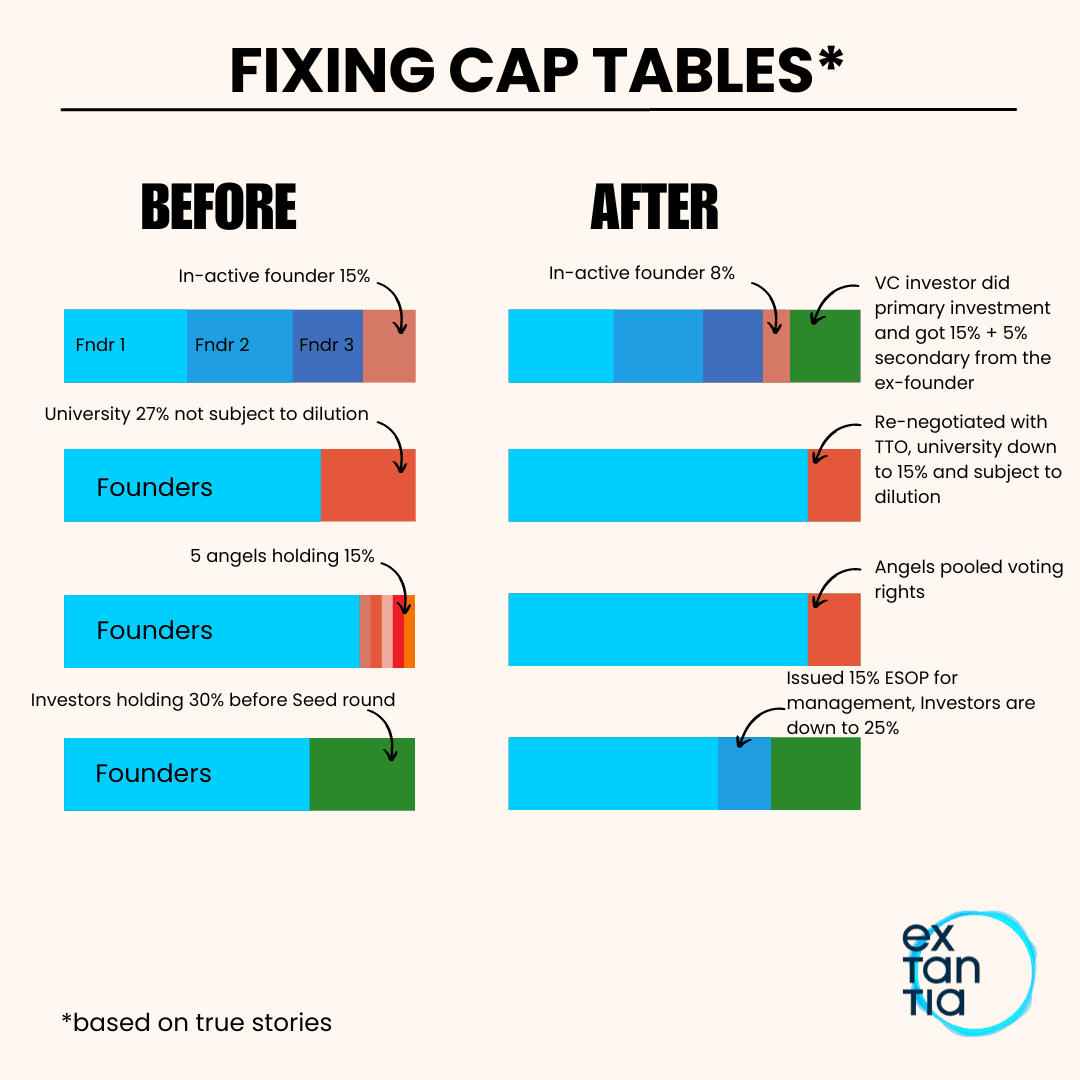

Fixing a messed up cap table

You’ve done your best to avoid all the pitfalls but still ended with a complex captable? Don’t worry. This is not the end of the stroy. True, cleaning up a messy cap table is a daunting task, but it's not impossible. It may involve difficult conversations and negotiations, but it’s in everyone's best interest to ensure the company is in a position to succeed.

First, analyse your current cap table structure. Understand who holds what, and whether there are any special rights attached to those holdings.

Next, start a dialogue with the relevant parties. If there are dormant shareholders, explore options such as buybacks, secondaries, or stock dilution. Negotiating with universities, accelerators, or angel investors may be necessary to balance the cap table in favour of the executive team and future investors.

In some cases, a complete recapitalisation may be required to fix a messy cap table. While this process can be complex, involving reissuing shares or creating a new class of stock, it can be the best way to reset the cap table in a manner that aligns with the future success of the company.

Engage your lawyers and tax advisors in these disucssions. Most of the time, the biggest hurdle to fix a cap table is tax considerations (shifting share ownership is not free…).

Remember, the goal of a clean cap table should be to create a capital structure where everyone's interests are aligned towards building the future success of the company.

So what?

A clean cap table is more than just an administrative detail; it’s a strategic asset that can significantly influence the future success of a startup. By ensuring that equity is distributed in a way that motivates the executive team and facilitates effective decision-making, you can position your startup for success. While cleaning up a messy cap table can be a challenging task, it is an investment in the future of the company that can pay dividends in the long run.

In this context, always remember the second law of thermodynamics - it is extremely difficult to undo a mess. So, strive to get it right from the get-go.