" height="271.9999926478547px" id="EEb7rlRyU" width="823.9999863254119px"/><path d="M 41.234 82.42 C 64.009 82.42 82.469 63.97 82.469 41.21 C 82.469 18.451 64.009 0 41.234 0 C 18.461 0 0 18.451 0 41.21 C 0 63.97 18.461 82.42 41.234 82.42 Z" fill="rgb(20, 232, 155)" height="82.4204655951471px" id="oKwt2AI3_" transform="translate(545.508 14.698)" width="82.46885142513122px"/></g></svg>)

How we calculate emissions reduction potential: updated guidance from Project Frame.

At Zero Carbon our investment thesis is to invest in scientist entrepreneurs building solutions to the biggest unsolved problems of climate change. Our focus is on decarbonisation, and so for each investment we look for an Emissions Reduction Potential of half a gigatonne of carbon dioxide per year by 2050 (i.e. 0.5 GtCO₂e/year), roughly equivalent to 1% of global annual emissions in 2025. I’ve written about our thesis and methodology previously here.

Whilst we have our own targets, and build our own theories of change about how a technology will have an impact, we aim to follow best practices in performing our calculations. To that end, we are a member of Project Frame and contributor to the content working group that develops the guidance. Our investment thesis was strongly influenced by Pippa’s early experience angel investing alongside Prime Coalition, which (alongside NYSERDA) published the first Emissions Reduction Potential (ERP) methodology in late 2017.

About Frame

Project Frame is a community, convened by Prime Coalition, that aims to accelerate investment in climate by demystifying the climate impact assessment process. Building common terminology, methodology, and best practices while centering transparency and accountability. Project Frame currently represents over 900 individuals and over 365 investment firms representing $670B in assets under management.

Project Frame published some initial guidance in 2023 which set out the shared nomenclature and methodology. Project Frame published their most recent update to the methodology in late 2024, making it more accessible to investors new to the idea of pre-investment impact assessment and deepening the guidance around unit impact calculations. Here I just want to highlight some of the latest additions, what it means for pre-investment impact assessment, and point founders and fellow investors towards the new guidance and tools for calculating impact.

The new guidance is way more fleshed out for investors/founders/LPs that are new to pre-investment impact assessment

The team have added some additional resources include Foundational Best Practices which answers questions like: What are emissions factors? What is global warming potential (GWP)? What are common errors made as analysts move through the quantification process?

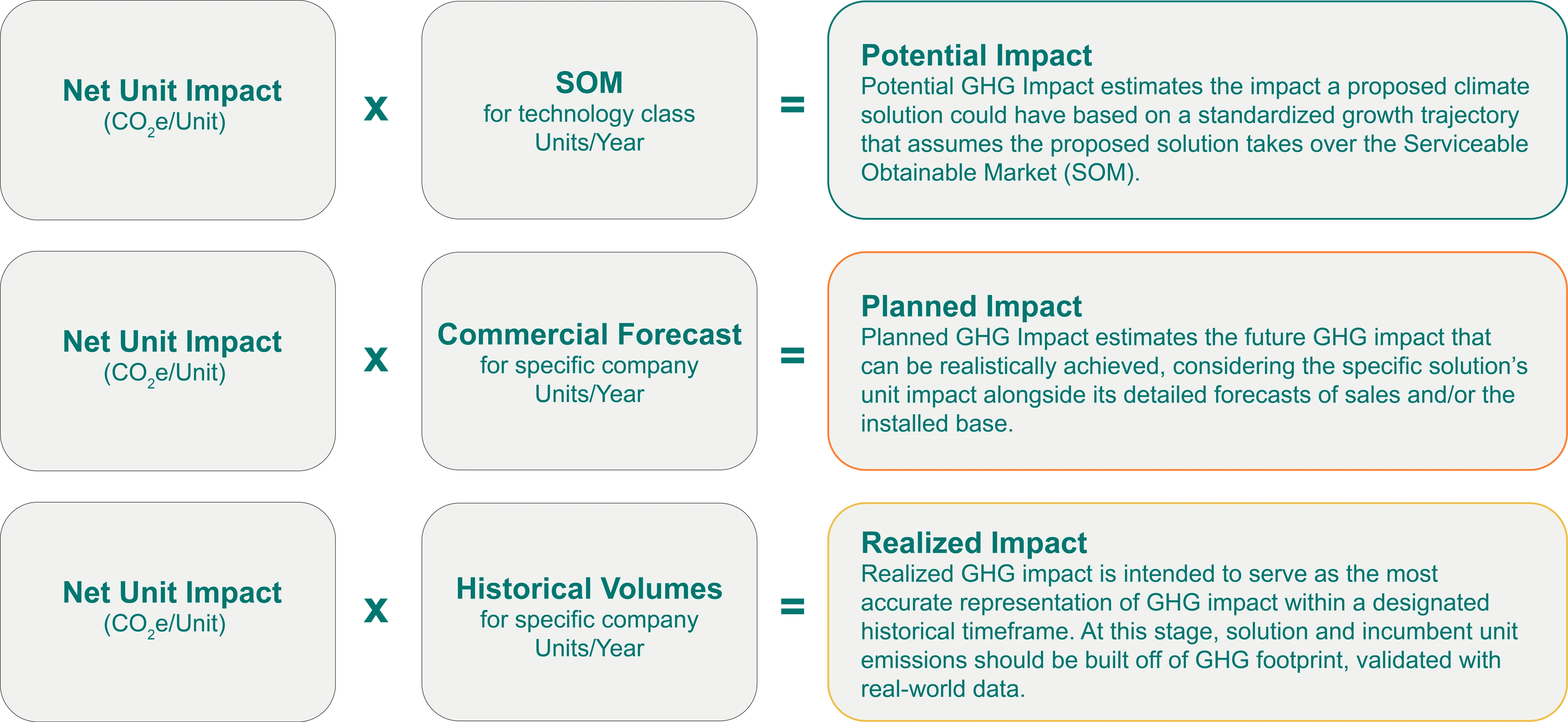

As before, the central equation for calculating impact involves calculating the unit impact (the difference in emissions between a new technology vs the incumbent technology) and multiplying it by the market size.

The core equation used by the methodology for determining impact, which new, optional adjustment factors.

New in 2024 is the inclusion of optional adjustment factors to give adjusted GHG impact. The most commonly used adjustment factor is in accounting for the Rebound effect (also referred to as Jevon’s Paradox), where an improvement in technology might lead to a reduction in unit impact, but lower costs/improved efficiency results in higher volumes, which in turn increase emissions (and thus reduce the impact). A recent example here is LED light usage: whilst LED lights are drastically more energy-efficient that their luminescent counterparts, the potential emissions reduction gains have been slightly reduced because we haven't replaced them one for one, but rather more LEDs have been installed than otherwise would have, because of the cheaper running costs afforded by efficiency improvements. Data centre energy efficiency is another example – if chips and/or data centre cooling gets more efficient and therefore cheaper, we are likely to just enable more computers.

Pre-investment impact measurement is divided into top-down or bottom-up estimates for market sizing, depending on the technology maturity. At Zero Carbon we calculate Emissions Reduction Potential, which in Frame terminology is Potential Impact – we take a top-down approach to calculating how big the problem is currently, and what the maximum impact would be if a company took the entire market. We don’t necessarily expect them to do so, but it allows us to imagine that the company could have a sizeable impact even if they took a portion of that market.

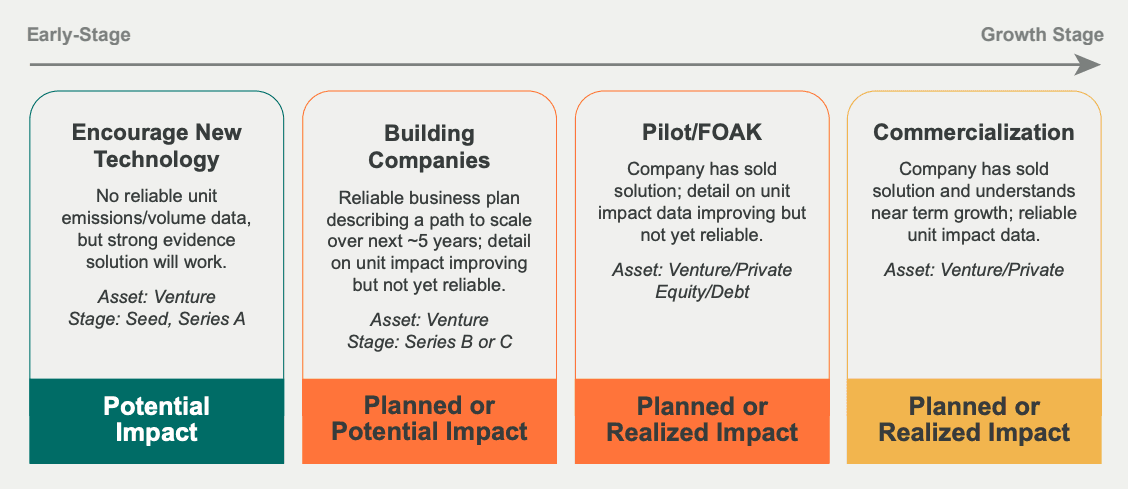

Once a technology is de-risked and is close to entering the market, with realistic commercial forecasts, then a bottom-up calculation of Planned Impact becomes more appropriate. In the latest methodology guidance, Project Frame have illustrated where investors typically use Potential and Planned impact. And of course, once these technologies are deployed at scale, companies and investors can started to measure Realized Impact—this is an area where guidance is still being developed, and we look forward to learning more as our companies grow and start to realise their potential.

The type of impact calculations usually employed by investors as a function of stage. As (pre-)seed investors at Zero Carbon, we use potential impact as our metric to evaluate investments.

The case studies are excellent

Not sure about how investors arrive at a number for emissions reduction potential? Or what assumptions they’re making about market sizing, growth, grid emissions intensities? Project Frame have added Case Studies, inspired by real investments, for everything from green ammonia production to heat pump installation so you can see how the methodology is used in practice. (And of course, the CRANE tool also has even more case studies. The CRANE tool is an open access tool that implements the Frame methodology with 200+ pre-filled models). If you’re reading this as a seasoned climate tech investor—consider contributing to future case studies yourself.

There are still some open questions

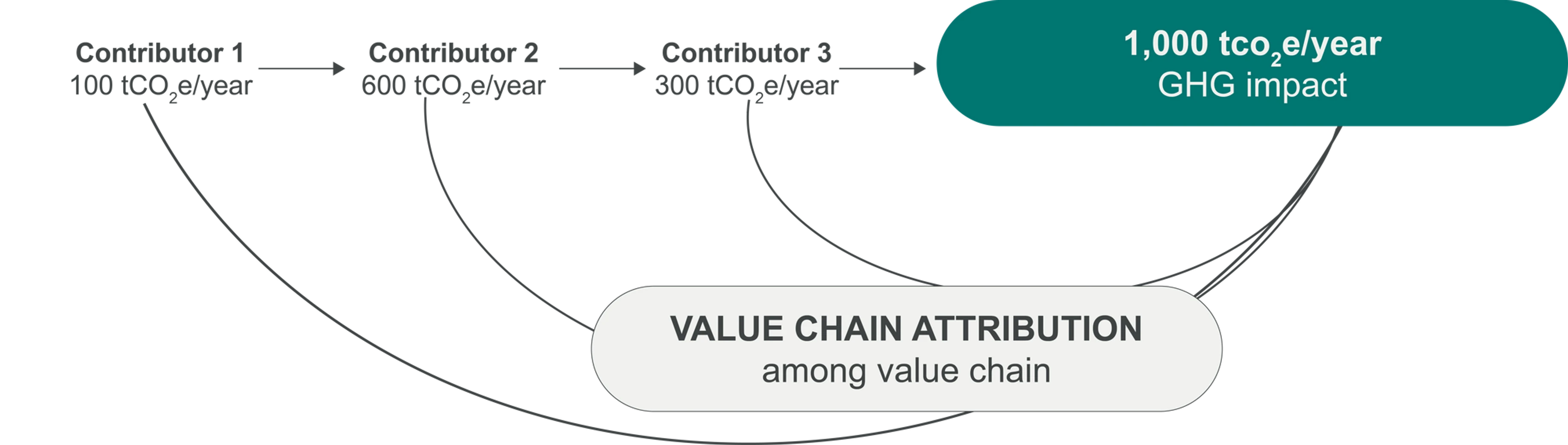

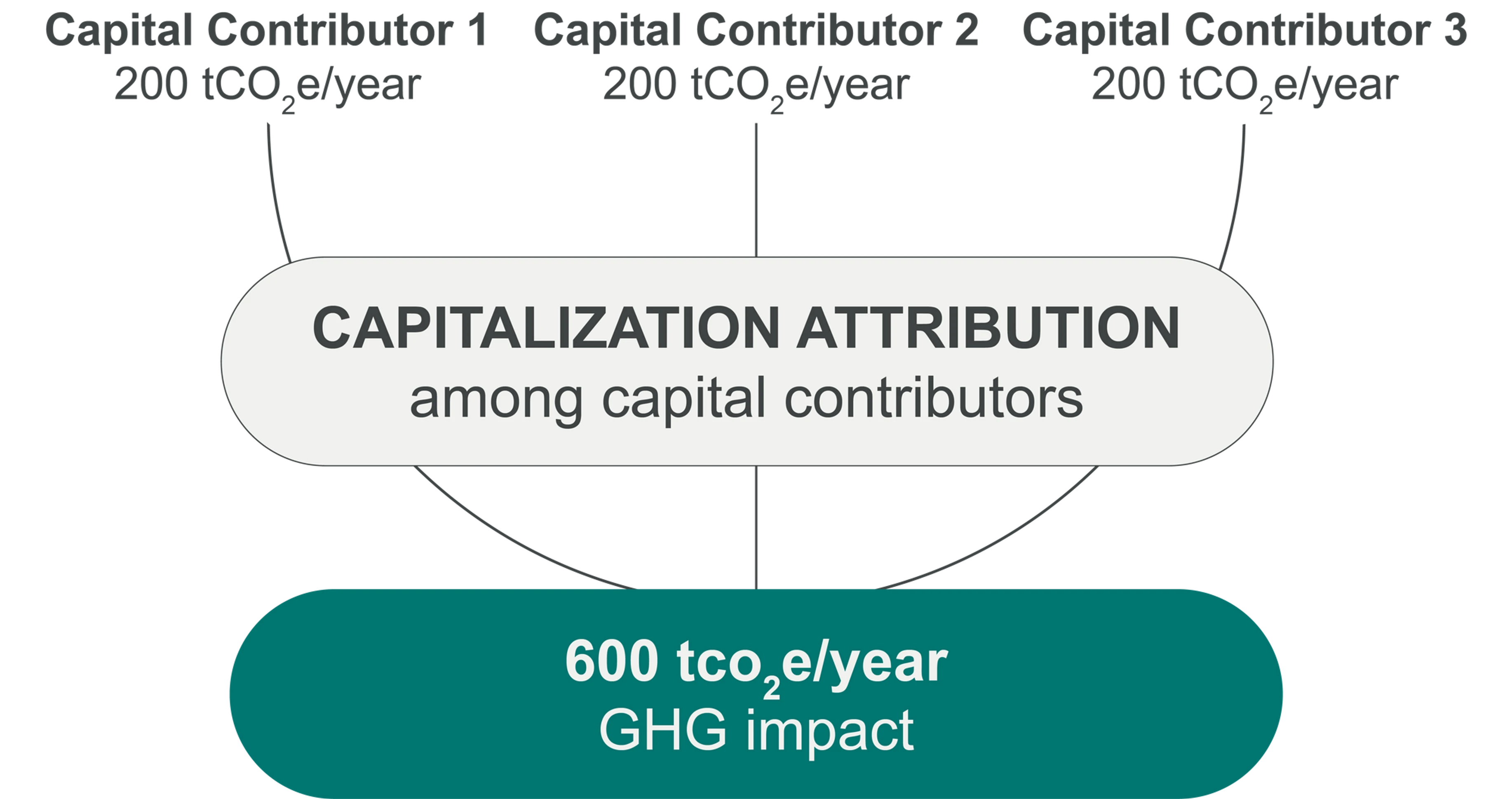

Attribution is an area of discussion within the Frame community. Attribution refers to how much of the impact can one actor claim e.g. one solution in a value chain, or one investor in a syndicate. The Project Frame guidance does not provide a recommendation as to whether or not investors should attribute impact in their reporting, but guidance exists on terminology should they wish to.

Value chain attribution: attributing portions of emissions reduction impact across contributors along the value chain.

Capitalization attribution: attributing portions of emissions reduction between investors and other capital contributors.

Additionality continues to be a hotly debated topic: what would happen in the absence of that particular investment? Can it claim to be additional? The latest definition from Project Frame is as follows: “An attribute of impact requiring an investor or company’s thoughtful and reasonable articulation of the degree to which its support causes a change in an outcome that would have not otherwise happened (in a no-intervention or business as usual baseline scenario).” Some believe that additionality is a pre-requisite for measuring impact, whereas others argue that you can have impact with and without additionality. There is more detail in the guidance if you want to learn more about this topic.

Later stages Project Frame is looking to extend its guidance to later stages of investment. For us at ZCC this will be extremely useful for our portfolio companies as they grow and work to define their impact for later stages. It also helps us to build theories of change and ERP calculations to be transferable to later stage investors as our companies grow.

We hope this offers some useful tips to founders developing their Emissions Reduction Potential estimates. Check out the full guidance (Evaluating Greenhouse Gas Impact for Early-Stage Investments) for more in-depth detail on calculating unit impact and market sizing.

Want to keep up to date with the latest guidance in impact assessment? Join the Project Frame community!